ICICI Bank Q3 Results 2026: Profit, NII, Asset Quality & Key Financial Highlights Explained

By Kaushik Brahmakshatriya

Published On 19 April 2026.

ICICI Bank Q3 Results 2026: Strong Growth Across Key Metrics

ICICI Bank Ltd has once again delivered a solid quarterly performance in Q3 FY2025-26, showcasing strong growth in profitability, stable asset quality, and consistent expansion in its loan book. The bank continues to strengthen its position as one of India’s leading private sector banks, driven by robust retail lending and improving operational efficiency.

Key Financial Highlights (Q3 FY2026)

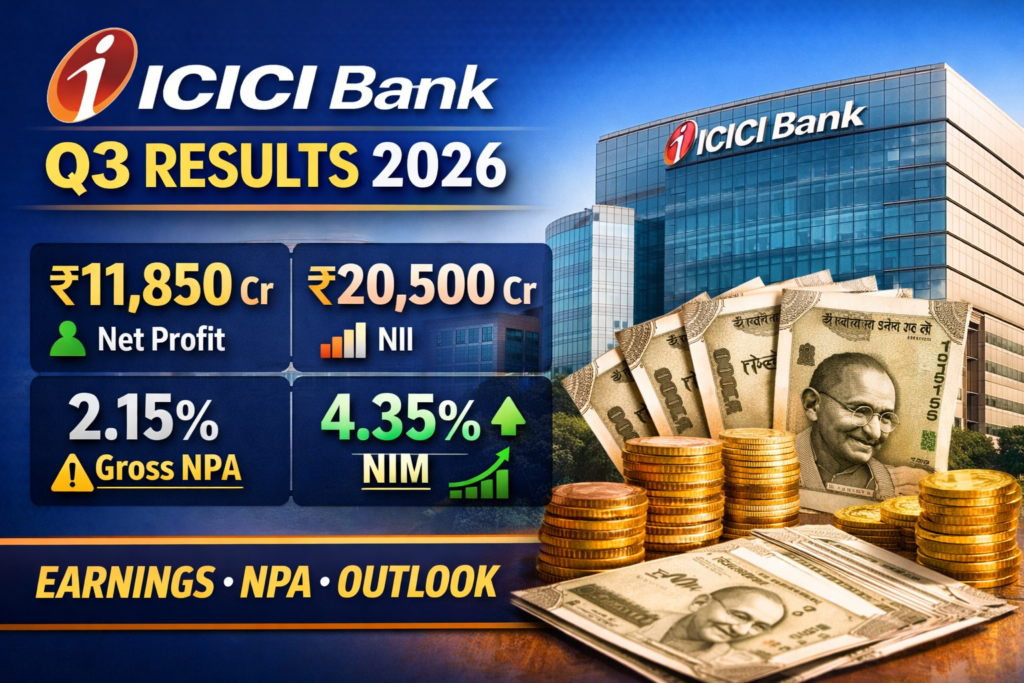

*Net Profit: ₹11,850 crore (YoY growth of ~18%)

* Net Interest Income (NII): ₹20,500 crore (YoY growth of ~14%)

* Total Income: ₹45,200 crore

* Operating Profit: ₹16,900 crore

* Net Interest Margin (NIM): 4.35%

* Gross NPA: 2.15%

* Net NPA: 0.42%

* Provision Coverage Ratio (PCR): 80%+

* CASA Ratio: 43.5%

These numbers indicate strong earnings momentum along with controlled risk levels.

Profit Growth Analysis

ICICI Bank reported a net profit of ₹11,850 crore, marking a significant increase compared to the same quarter last year. The steady rise in profitability is mainly driven by:

* Growth in retail loan portfolio

* Higher interest income

* Controlled operating expenses

* Lower credit costs

The bank has maintained a consistent upward trend in quarterly profits, reflecting strong management execution and favorable macroeconomic conditions.

Net Interest Income (NII) & Margins

The Net Interest Income (NII) stood at ₹20,500 crore, showing a healthy year-on-year growth of around 14%.

* Net Interest Margin (NIM): 4.35%

This indicates efficient lending practices and a strong balance between deposit and lending rates.

ICICI Bank continues to benefit from:

* Strong retail loan demand

* Better yield on advances

* Stable cost of funds

Loan & Deposit Growth

Loan Book Growth:

Total advances grew by approximately 17% YoY

Retail loans contributed over 53% of the total portfolio

Key segments driving growth:

* Home loans

* Personal loans

* Auto loans

* SME financing

Deposit Growth:

* Deposits increased by 14% YoY

* CASA deposits remained strong, improving liquidity and reducing funding costs

Asset Quality Improvement

Asset quality remains one of the strongest aspects of ICICI Bank’s Q3 results.

Gross NPA: Reduced to 2.15%

Net NPA: Declined to 0.42%

This reflects better risk management and recovery mechanisms.

Key Highlights:

* Decline in slippages

* Strong recoveries and upgrades

* Lower provisioning requirements

The Provision Coverage Ratio (PCR) above 80% ensures that the bank is well-protected against potential future losses.

Operating Performance

Operating Profit: ₹16,900 crore

Cost-to-income ratio remained under control

The bank has improved efficiency through:

* Digital banking expansion

* Automation of processes

* Reduced operational costs

Digital Banking Growth

ICICI Bank continues to invest heavily in digital transformation:

* Increased usage of mobile banking apps

* Growth in online transactions

* Expansion of digital lending platforms

Digital channels now contribute a significant portion of new customer acquisitions and transactions.

Segment Performance

Retail Banking:

Strong demand across loans

Stable asset quality

Corporate Banking:

Balanced exposure with improved credit monitoring

Treasury:

Contributed steadily to overall income

Key Ratios Summary

| Metric | Q3 FY2026 |

| Net Profit | ₹11,850 crore |

| NII | ₹20,500 crore |

| NIM | 4.35% |

| Gross NPA | 2.15% |

| Net NPA | 0.42% |

| CASA Ratio | 43.5% |

Management Commentary (Summary)

The management of ICICI Bank highlighted:

Continued focus on sustainable growth

* Maintaining strong asset quality

* Leveraging technology and digital platforms

* Expanding retail and SME segments

* The bank remains optimistic about future growth despite global economic uncertainties.

Future Outlook

Looking ahead, ICICI Bank is expected to:

* Maintain strong credit growth

* Focus on retail and digital banking expansion

* Keep asset quality under control

* Improve profitability further

* With India’s economic growth remaining strong, the bank is well-positioned to benefit from rising credit demand.

Conclusion

The Q3 FY2026 results of ICICI Bank reflect a balanced and strong financial performance. With rising profits, stable margins, improving asset quality, and continued digital expansion, the bank has reinforced its leadership in the Indian banking sector.

For investors and analysts, ICICI Bank remains a solid long-term bet due to its consistent performance and prudent risk management strategies.

Disclaimer

This blog does not provide financial, investment, or trading advice. All content is for educational and informational purposes only. Please consult a certified financial advisor before making any investment decisions. The author will not be responsible for any financial losses incurred